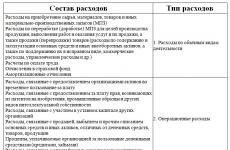

Thin capitalization rules using an example. Press about you RF. Thin capitalization in NK

The term “thin capitalization” characterizes the financial condition of a company when the amount of borrowed funds significantly exceeds its equity capital. In this case, the company’s activities are financed not by investments of its owners in the authorized capital, but by attracting debt financing. In some countries, this may be considered as a method of tax optimization or even an attempt to evade paying taxes.

After all, interest on borrowed funds paid to the lender reduces the tax base for income tax, and the national legislation of some countries may provide for “preferential” taxation of interest received compared to dividends.

Thin capitalization in NK

The Tax Code does not contain the term “thin capitalization”. At the same time, the rule of “thin capitalization” is laid down in paragraph 2 of Art. 269 of the Tax Code of the Russian Federation and concerns the calculation of the maximum amount of interest on debt obligations included in expenses when calculating income tax in certain cases (Letter of the Ministry of Finance of Russia dated September 17, 2013 No. 03-08-05/38346).

In what cases does the “thin capitalization” rule apply?

The thin capitalization rule applies to a Russian entity in relation to its controlled debt to a foreign entity. Such controlled debt represents a debt obligation that arose before:

- a foreign organization that directly or indirectly owns 20% or more of the authorized capital of this Russian organization;

- a Russian organization recognized as an affiliate of the above-mentioned foreign organization;

- other organizations, but the above-mentioned foreign and Russian organizations act as a guarantor, guarantor for such a debt obligation, or otherwise ensure the fulfillment of such an obligation.

How does the thin capitalization rule work?

In relation to controlled debt, which exceeds the equity capital of the Russian borrowing organization by more than 3 times, the organization can recognize a limited amount of interest as expenses for income tax purposes. It is calculated in a special manner, which we discussed in

In the Russian Federation, the taxpayer's debt is subject to control. Once it exceeds the limit (measured by the ratio of equity to debt), a tax is levied. Thin capitalization is a concept associated with the timely payment of loan interest (dividends in favor of foreign legal entities) by Russian companies. Under the guise of interest payments on debts, profit distribution is possible. The purpose of this operation by a resident taxpayer is to withdraw capital abroad without taxation, as a result of which the country’s budget suffers.

International agreements, norms and the fight against “thin capitalization” do not regulate. And in the legislation of the Russian Federation there is no concept of “thin (insufficient) capitalization,” making it difficult to apply international standards. In the Tax Code of the Russian Federation, the rules of thin capitalization are defined in paragraphs 2-13 of Article 269. Also regulated by the Transfer Pricing Guidelines for Multinational Tax Entities.

Strictly economically, the concept combines rules to combat the distribution of dividends hidden as interest for affiliates. In international financial practice, taxes on dividends are usually higher than taxes on interest on borrowed funds. Therefore, the company must pay both income taxes (in the Russian Federation - 20%) and taxes on dividends (13%). When paying interest, you are required to pay one tax, calculated according to the rules of another state (going to the budget of that state).

If foreign company A wants to invest in domestic company B, for example, 100 million rubles, then A can invest in the authorized capital of B and pay a tax of 20%. When paying dividends A, a tax (15%) will be withheld, which will be reduced if the Russian Federation has a Double Taxation Agreement with country A. But A can do differently - issue a loan to B (it is enough to create a company, for example, with an authorized capital of 10,000 rubles). The interest paid by A will reduce the income tax. Thin capitalization rules protect against artificial schemes to reduce revenues to the Russian budget.

The borrower and lender may even be “subsidiaries” of a third company or holding company. Reclassification of all (part of) interest as dividends is possible only if there is interdependence between the lender and the borrower. Interest from a borrower from the Russian Federation to a foreign lender can be considered as dividends when taxing the source of payments.

The taxpayer may have problems streamlining the calculation of debt, taxation of amounts exceeding the maximum interest rate for capitalization.

Types of controlled debt

These include loans issued:

- a domestic company – an affiliate of a foreign one;

- a foreign company owning (possibly indirectly) more than 20% of the authorized capital of a Russian company;

- to any person if a foreign company (affiliated person from the Russian Federation) acted as a guarantor or surety of a Russian company.

Interest - to the lender. If this is the parent company, everything is clear. If the interest is paid to an affiliate of the parent company, the payments are not dividends (“no share in the capital - no claim to profit”).

Taking advantage of the imperfection (uncertainty) of the concept of thin capitalization, transnational corporations withdraw their profits from Russian jurisdiction. They do not pay all taxes, issuing new loans to Russian companies instead. There are judicial precedents in the Arbitration Court on the reclassification of interest as taxable dividends, as well as on insufficient capitalization.

Thin capitalization rules, the essence of thin capitalization from a tax point of view, tax authorities’ arguments, main trends in 2016 and changes in 2017.

Thin capitalization from a tax perspective

The term thin (insufficient) capitalization characterizes the financial condition of a company when the amount of borrowed funds significantly exceeds its equity capital. In this case, the company's activities are financed not through investments of its owners in the authorized capital or assets, but through borrowed financing.

In many countries, thin capitalization is seen as an attempt to evade paying taxes, primarily income tax. Thus, the letter of the Ministry of Finance of the Russian Federation dated May 26, 2010 No. 03-08-05 explains the meaning of thin capitalization, indicating that the application of thin capitalization rules is aimed at combating tax abuses in the hidden distribution of dividends under the guise of interest payments between affiliates. In this case, the borrower and the lender must be affiliated directly with each other or both with third parties. Interest is not reclassified as dividends if there is no relationship of interdependence between the borrower and the lender.

In Russia, the thin capitalization rule is formulated in subparagraphs 2-13 of Article 269 of the Tax Code of the Russian Federation, which regulate controlled debt to a foreign organization.

Thin capitalization rules for corporate income tax

The thin capitalization rule applies to a Russian entity in relation to its controlled debt to a foreign entity. The corresponding debt obligation must arise, as of the current date, before:

- a foreign organization that directly or indirectly owns 20% or more of the authorized capital of this Russian organization (from January 1, 2017 - 25%);

- a Russian organization recognized as an affiliate of the above-mentioned foreign organization;

- other organizations to which the above foreign and Russian organizations act as surety, guarantor or otherwise ensure the fulfillment of a debt obligation.

For controlled debt that exceeds equity Russian borrower by more than 3 times (for banks - 12.5 times), the organization can recognize a limited amount of interest (marginal interest) as expenses for profit tax purposes. This amount is determined on the last day of each reporting (tax) period.

Discriminatory nature of Russian rules on thin capitalization

The institution of thin capitalization, not least due to the insufficiently clear wording of Article 269 of the Tax Code of the Russian Federation, in practice has given rise to many questions. One of the most important problems was the relationship between Article 269 of the Tax Code of the Russian Federation and the provisions of international treaties, which, according to Part 4 of Article 15 of the Constitution of the Russian Federation, have priority over the norms of the Tax Code of the Russian Federation.

According to Article 24 of the Model Convention of the Organization for Economic Co-operation and Development (OECD MC), the non-discrimination provisions, which are common to most double tax treaties concluded between the Russian Federation and other countries, prohibit discrimination of capital both on the basis of the recipient of interest and on the basis of a sign of control of the capital of the payer of interest by the recipient-creditor (clauses 4 and 5 of the article).

It should be noted that the taxpayer was not helped either by the explanations of the Ministry of Finance, or by a judicial act previously adopted in his favor on similar factual circumstances (Resolution of the Federal Antimonopoly Service of the Moscow Region dated December 8, 2010 No. KA-A40/14266-10 in case No. A40-15966/10-114- 99 - the famous Scania Leasing case).

Formal Approach to Applying the Debt to Equity Ratio

If the equity value is negative, the entire amount of interest on controlled debt is equal to dividends and is subject to taxation in accordance with Art. 284 of the Tax Code of the Russian Federation, and not only in terms of the excess over the market price of the loan. This position is set out in the letter of the Ministry of Finance dated May 30, 2011 No. 03-03-06/1/319. In particular, this approach was supported by the court in the Megapolis case (Resolution of the Arbitration Court of the Moscow Region dated 04/05/2016 No. F05-20982/2015 in case No. A40-81712/2015).

Thus, by applying a formal approach and distorting the legal rules, law enforcement agencies reduce the ability of the taxpayer to prove that he acted according to the arm's length principle with a negative net worth, and impose tax on the entire amount of payments, instead of the difference between the amount of interest and the market value of the loan.

Main trends in law enforcement practice in 2016

In addition to the above judicial acts, a varied practice developed in 2016.

1. The lack of a uniform approach on some issues creates legal uncertainty for taxpayers. Thus, in the “Arctic Gas Company” case (resolution of the AS ZSO dated 04/07/2016 No. F04-852/2016 in case No. A81-3540/2015), the court came to the conclusion that the obligation established by Article 296 of the Tax Code of the Russian Federation to calculate maximum interest and withhold tax from source from amounts exceeding such percentages (dividends) is associated with the fact of transfer of these amounts, while in the case of “Scania Leasing 2” (resolution of the Arbitration Court of the Moscow Region dated September 14, 2016 No. F05-13038/2016 in case No. A40-149755/2015) the court supported the tax authority’s argument that the obligation to calculate maximum interest does not depend on the actual payment of amounts to an interdependent non-resident, i.e. outstanding interest is also the basis for applying the rules of Art. 269 of the Tax Code of the Russian Federation.

The Scania Leasing 2 case turned out to be rich in “harsh” conclusions from the tax authority. Thus, the court recognized that, regardless of the formation of the tax base in the jurisdiction of the lender, if corporate debt is serviced through the redistribution and withdrawal of profits received in the Russian Federation, this is in the nature of a “scheme” associated with obtaining an unjustified tax benefit.

2. The business purpose of the transaction is at the forefront. Considering the issue of sister company under loan agreements, the court found it unlawful to include the corresponding amounts in the loss of the assignor bank. The court indicated that since no measures were taken to settle the debt (collection of collateral) by the bank, the transaction had no business purpose other than the transfer of interest from the bank's borrowers through the Russian sister company of the parent company located in Cyprus. The tax authority proved that the sister company is an SPV (case "Yuriastrum Bank" - resolution of the Arbitration Court of the Moscow Region dated October 5, 2016 No. F05-14375/2016 in case No. A40-63455/2015).

3. Positive points. When considering the issue of the procedure for withholding tax at the source of payment by a tax agent, the court recognized that Article 269 of the Tax Code of the Russian Federation has priority over the provisions of Article 310 of the Tax Code of the Russian Federation, regarding the procedure for fulfilling the obligation to withhold tax by a tax agent. In the same case, the taxpayer was helped by a letter from the Federal Tax Service, received before the controversial periods and addressed to the taxpayer on a specific issue. The letter protected the organization from the conclusions of inspectors made as part of a tax audit (the Shcheleyki Quarry case - resolution of the AS SZO dated September 22, 2016 No. F07-7001/2016 in case No. A56-47615/2015).

Considering the issue of debt forgiveness by a non-resident lender, the court indicated that debt forgiveness within the amount of accrued interest is not the income of the lender, and in such a situation, Art. 269 of the Tax Code of the Russian Federation does not apply (the “Arcticneft” case - resolution of the AS SZO dated April 22, 2016 No. F07-1186/2016 in case No. A05-13582/2014).

Thin capitalization rules - 2017

On January 1, 2017, the changes introduced by Federal Law No. 25-FZ of February 15, 2016 “On Amendments to Article 269 of Part Two of the Tax Code of the Russian Federation regarding the definition of the concept of controlled debt” (hereinafter referred to as “Law No. 25-FZ”) will come into force. ), which, according to the developers of the amendments, are introduced to eliminate unjustified tax burdens in certain cases.

Law No. 25-FZ introduces the following fairly significant changes:

1. The minimum threshold for participation in the capital of a taxpayer by foreign entities is determined in accordance with the rules of the Tax Code of the Russian Federation on interdependence (Article 105.1 of the Tax Code of the Russian Federation). This means that loans from any foreign persons are recognized as controlled debt if the share of direct or indirect participation of any foreign person (individual or legal entity) in both the Russian borrower and the foreign lender is more than 25% (versus 20% in 2016). ) or if the share of direct participation of each previous person in each subsequent organization is more than 50%.

2. An approach is being institutionalized, according to which debt to a foreign “sister” company is recognized as controlled. The approach was previously used by the courts, for example, in the Naryanmarneftegaz cases (Resolution of the Federal Antimonopoly Service of the Moscow Region dated February 27, 2012 No. F05-14903/2011 and Determination of the Supreme Arbitration Court of the Russian Federation dated 21 June 2012 No. VAS-7104/12), "Achimgaz" (Resolution of the Autonomous District of the Moscow Region dated 04/13/2015 in case No. A40-41135/14), "Air Gate of the Northern Capital" (Resolution of the Autonomous District of the North-Western District dated 06/19/2015 in the case No. A56-41307/2014).

3. The right of the court to recognize as controllable the outstanding debt of a Russian resident on debt obligations not specified in Art. 269 of the Tax Code of the Russian Federation. For such recognition, the court must establish that the ultimate purpose of payments for such obligations is payments to non-residents and their to related parties .

4. Since 2017, interest on domestic loans is not subject to rationing if the funds were received not as a loan from a foreign entity that owns the debtor by more than 25 percent, but on other terms. This resolves the situation where the participation criteria are formally met, but interest is not paid. However, the question of what rules apply if a Russian company transfers funds received from an interdependent “foreigner” to another Russian group company is still unresolved.

5. The following debts are not considered controlled:

- to foreign organizations that are issuers of marketable bonds (including Eurobonds) or recipients of interest income on them. The new rule consolidates the approach taken by the court in the Topaz Distillery case (Resolution of the 9th AAC No. 09AP-58460/2014);

- to Russian persons who are related to non-residents, provided that such Russian persons do not have comparable outstanding debt to a non-resident who is related to the borrower;

- to a bank independent of the Russian organization and persons ensuring the fulfillment of the obligation (guarantors, guarantors, etc.), provided that from the moment the obligation arose, neither the non-resident nor the persons ensuring the fulfillment of the obligation and the persons interdependent with him have not repaid this obligation. This rule has actually been applied since January 1, 2016.

conclusions

1. Based on the above innovations, we can conclude that thin capitalization rules are gradually becoming more widely used and are participating in the formation of a new complex set of rules on deoffshorization in terms of the mechanism that ensures taxation at the source of income. The main subject of the inspectors' analysis is not the conditions for issuing loans, but the figure of the final creditor - the beneficiary of the interest.

2. Taking into account paragraph 5 of Article 24 of the OECD MC and comments to it, we can conclude that paragraphs 2-4 of Article 269 of the Tax Code of the Russian Federation conflict with the prohibition of discrimination based on the place of origin of capital established by paragraph 2 of Article 3 of the Tax Code of the Russian Federation. The above amendments do not solve this problem.

3. Russian courts justify the application of Article 269 of the Tax Code of the Russian Federation by (often distorted) interpretation of the provisions of international treaties in their own interests, while official interpretations of the OECD Model Convention are used selectively.

4. Significant payments to non-residents within a group of companies will, if they fall under the criteria of the updated Article 269 of the Tax Code of the Russian Federation, be potentially risky.

Despite the removal of some financing transactions from control, the relaxations are negated by the court’s right to recognize any debt as controllable. Investing through intra-group loans, even at market interest rates (subject to the arm's length principle), requires increasingly careful analysis against the backdrop of ever-increasing risks.

Svetlana Belyaeva,

Tax Manager, Ex-Deloitte

Thin capitalization are rules that limit the possibility of hidden distribution of dividends under the guise of paying interest on debt obligations between affiliates.

To determine the maximum amount of interest recognized as an expense for tax accounting purposes, we will take the following steps:

STEP 1 We check whether the debt under the debt obligation is controllable. Controlled debt is an outstanding debt under a debt obligation in one of the cases provided for in criterion 1: CRITERION 1

- To a foreign company directly or indirectly owning more than 25% of the borrower's authorized capital

- Before a Russian company that is an affiliate of the above-mentioned foreign organization

- For a loan or credit, if such an affiliate or directly a foreign company acts as a guarantor, guarantor or otherwise undertakes to ensure the fulfillment of a debt obligation.

CRITERION 2 The amount of debt is more than 3 times the amount of equity capital of the Russian taxpayer organization.

For tax accounting purposes, equity is the difference between assets and liabilities (excluding tax liabilities).

That is, equity is calculated as:

SC = Total assets – Total liabilities + Tax liabilities

If the taxpayer, a Russian company, has controlled debt (CRITERION 1 is met) and the amount of this debt exceeds equity capital by more than 3 times at the end of the reporting period, then the thin capitalization rule is applied.

STEP 2 Calculate Capitalization Ratio Kk = Amount of controlled debt / (SC * Ownership share of the management company * 3),

where Kk is the capitalization ratio

Ownership share of a management company is the share of direct or indirect participation of a foreign organization in the authorized capital of a Russian organization.

STEP 3 Calculate the actual amount of accrued interest STEP 4 For the last day of the reporting (tax) period, we determine the maximum amount of interest included in expenses for tax accounting purposes: Maximum amount of interest = Accrued interest / Kk

STEP 5 The positive difference between accrued interest and maximum interest is equated for tax accounting purposes to dividends paid to a foreign organization. The amount of such dividends is taxed at a rate of 15%. Example The Russian company Karandash owns 70% of the shares of the Lastik company, and the foreign company Sticker owns 80% of the shares of the Karandash company.

The following information is available on the Lastik company as of March 31, 2018:

02/28/2018 the Karandash company provided a loan of 40,000,000 rubles to the Lastik company. at a rate of 25% per annum.

(a) Determine the maximum amount of interest that will be recognized in tax accounting as of March 31, 2018.

(b) Calculate the amount of interest recognized as dividends and the tax on dividends.

Solution We check the fulfillment of both criteria. The Sticker company indirectly owns the Lastik company and the share of such ownership is:

80% * 70% = 56%

That is, criterion 1 is met: the share of ownership (direct or indirect) of a foreign company by a Russian company is more than 25%.

Let us determine the amount of excess of the loan amount over the amount of equity capital (EK) of the Lastik company:

CK*3 = (100,000,000 – 95,000,000 + 3,000,000)*3 = 24,000,000< 40.000.000

Criterion 2 is also met and the loan size is more than 3 times the size of the insurance company.

Let's calculate the capitalization ratio Kk = Amount of controlled debt / (SC * Ownership share of the management company * 3)

Kk = 40,000,000 / (8,000,000 * 56% * 3) = 40,000,000 / 13,440,000 = 2.98 Let's calculate the actual amount of interest expenses 40,000,000 * 25% *31 / 365 = 849,315 rubles. Let's calculate the maximum amount of interest accepted for tax accounting purposes. Limit amount = Accrued interest / Kk

849.315 / 2.98 = 285.005 rub. Let us determine the amount of interest recognized as dividends and the tax on dividends. The amount of interest recognized as dividends for tax accounting purposes:

What is thin capitalization

An enterprise often attracts investments in the course of its activities. Sometimes the volume of these investments begins to exceed the size of their capital. Then such a concept as thin capitalization (TC) becomes relevant.

What is thin capitalization?

Thin, or insufficient, capitalization is a state of a company in which the amount of loans exceeds its capital many times over. That is, the activity of the enterprise is ensured not at the expense of the authorized capital, but at the expense of third-party sources. The concept of TC is used in many countries. In most countries, detected thin capitalization may raise suspicions of an attempt to evade taxes.

In this regard, there are rules of the Labor Code. Their essence, as well as the very definition of insufficient capitalization, is revealed in the letter of the Ministry of Finance No. 03-08-05 dated May 26, 2010. It states that these rules are necessary to prevent tax abuse. The latter may arise during the hidden division of dividends between participants. The company transfers dividends, but does so under the guise of paying off interest.

The rules for thin capitalization are established by Article 269 of the Tax Code of the Russian Federation. It regulates controlled debt to foreign companies. Paragraphs 2-4 of Article 269 indicate that special rules for calculating interest are established for firms with uncovered controlled liabilities.

IMPORTANT! The rules of the Labor Code apply when the debt exceeds more than 3 times the capital of the company. The amount of the latter is stated in line 1300 “Total for section 3” of the balance sheet. The amount of the company's tax debt is added to this value.

When does the thin capitalization rule come into play?

The Labor Code rule is relevant for Russian legal entities that have a controlled debt to a foreign company. Controlled debt implies obligations to the following persons:

- A foreign company that owns more than 25% of the borrower's authorized capital.

- A Russian legal entity considered to be dependent on a foreign company. It is assumed that this company owns more than 25% of the borrower's share capital.

- Other companies, if the persons specified in the previous paragraphs are the guarantor or guarantor for the debt.

The rule is relevant when the debt to the persons listed above exceeds the capital of the company itself by three times.

The essence of the thin capitalization rule

If related circumstances are found, the firm must recognize some amount of interest in its expense structure for tax purposes. This size is determined in a regulated manner, which will be given below.

If the interest on the debt is more than the established interest rate, the difference is considered dividends paid to the non-resident. These dividends will be subject to income tax. The rate is 15% based on paragraph 3 of Article 284 of the Tax Code of the Russian Federation. The tax is withheld by the borrower, who is considered a tax agent on the basis of paragraph 3 of Article 275 of the Tax Code of the Russian Federation.

How to calculate thin capitalization

The interest rate is determined at the closing date of the quarter or month. If a company takes out a loan in foreign currency, it must be converted into rubles in accordance with the Central Bank exchange rate on the day of transfer. The conversion of % into rubles is carried out in accordance with the exchange rate on the final day of the month for which they were accrued. To determine the amount of interest that needs to be taken into account in the cost structure, you must first determine the capitalization ratio. To calculate it, use this formula:

(Amount of liabilities (own capital * non-resident share) / 3)

The maximum interest amount is determined by this formula:

Interest per quarter or month / capitalization rate

Let's look at an example. The company has these financial characteristics:

- The share of participation of a foreign person is 50%.

- The amount of controlled debt is 1 million rubles.

- Interest for the third quarter is 10,000 rubles.

- The value of line 1300 of the balance sheet is 60,000 rubles, the credit balance of the account is 68 – 110,000 rubles. Equity is the sum of these values. That is, it will be 170,000 rubles.

First you need to determine the capitalization ratio: (1,000,000 (170,000 * 0.5) / 3). That is, the coefficient will be 3.92.

After this, you need to find the maximum interest amount: (10,000 / 3.92). The maximum amount of interest will be 2,551.02 rubles. That is, in the third quarter it is possible to take into account only 2,551 rubles. The balance will be 7,449 rubles (10,000 – 2,551). It cannot be included in the cost structure. This balance will be considered dividends. Taxes will be withheld from it.

IMPORTANT! In the event that the firm's capital volume is negative, both the coefficient and the interest limit will be zero.

Changes in laws in the field of thin capitalization in 2017

In 2017, some changes regarding the Labor Code came into force. They remain relevant in 2018. The adjustments were made on the basis of Federal Law No. 25 “On Amendments to Article 269 of the Tax Code of the Russian Federation” dated February 15, 2016. The regulatory act came into force on January 1, 2017. The main purpose of introducing changes is to prevent unjustified tax burden. Let's consider all the provisions established by Federal Law No. 25:

- The lowest threshold for the participation of a foreign legal entity in the company's share was 25%. Previously it was equal to 20%. This indicator is used to determine controlled debt.

- The judicial authority has the right to recognize as controllable the debt of a resident of the country for obligations not specified in Article 269 of the Tax Code of the Russian Federation. Debt is considered controlled if it has been established that the final purpose of payments on obligations is payments to foreign persons or legal entities dependent on foreign companies.

- Since 2017, interest on loans within the country does not need to be standardized. An exception is funds issued as a loan by a non-resident who owns more than 25% of the company.

The new law states that debts cannot be considered controlled if they are taken from the following persons:

- Foreign firms considered to be issuers of publicly traded bonds.

- Foreign firms receiving income from bonds.

- Banks, independent of the domestic company, ensuring the fulfillment of obligations by persons. Condition: the debt was not repaid either by the non-resident or by persons dependent on him.

Since 2017, laws have become more liberal. Some of the provisions (for example, the last one) were used secretly in 2016.

Using thin capitalization rules in practice

Legal entities must take into account the rules of thin capitalization. In particular, existing regulations make any significant payments sent to a foreign company a tax risk. The position of the courts must also be taken into account. As a rule, decisions are made in the direction of additional taxes.

In practice, courts often use the provisions of Article 269 of the Tax Code of the Russian Federation in their own interests. International treaties may be misinterpreted in these same interests. It must be taken into account that a huge part of payments to non-residents within one group may fall under the updated standards, that is, payments become risky.

Assistant - electronic magazine for small businesses, entrepreneurs, accountants, lawyers, personnel officers

- Labor productivityJanuary 8

- Tariff rates for underground miners in Kuzbass for 2019 January 6

- Purchasing through an individual entrepreneur - does it make sense? January 2

Ask a question on the forum Acts, Statements, Statements, Powers of Attorney, Job descriptions, Journals, Reports, Letters, Orders, Protocols, Certificates, Notifications and others. There are 784 documents in total.

- Insurance experience calculator and 8 more calculators.

- Production calendar 2019 and 3 more for regions.

- Minimum wage, subsistence minimum, KBK, OKVED and more.

If a Russian company has foreign owners, then when the need for financing arises, it would be wise to turn to them for help first, since foreign money, as a rule, is significantly cheaper than Russian money. A foreign owner has two main ways to help with financing: by contributing to the authorized capital or by providing a loan. What can a foreign investor expect in each of these cases and what will be the possible tax consequences?

Capital contribution

If financial assistance is provided in the form of a contribution to the authorized capital, then the investor can count on dividends as income on the invested money. Why are dividends bad? Firstly, a Russian company will be able to pay dividends only if it shows profit according to accounting data. Secondly, dividends will be subject to withholding tax. The tax rate will generally be 15% (i.e., out of 100 rubles of dividends due to a foreign shareholder, only 85 rubles will reach him, the rest will go to the Russian tax authorities). Double tax treaties between Russia and other countries often provide for a reduced tax rate on dividends (for example, 10% or even 5%), but to apply the reduced rate usually requires overcoming restrictions on the shareholding and the value of that share (for example, the treaty with Germany provides a reduced tax rate on dividends of 5%, provided that the German owner's share is at least 10% and is worth at least 80,000 euros). And thirdly, dividends will not allow a Russian company to save on income tax, since dividends do not reduce the taxable profit of the company paying them.

We do not mention here at all the legal side of the issue (the need to hold a general meeting and obtain the approval of participants/shareholders, make changes to the Charter, etc.)

Providing a loan

Against this background, a loan from a foreign owner looks like a more profitable financing option from a tax planning point of view. Interest is paid regardless of the company's profit. Most double tax treaties provide for the exemption of interest from withholding tax (i.e., if a foreign owner-creditor is owed 100 rubles of interest, then he will receive the full 100 rubles). In addition, the interest reduces the taxable profit of the Russian company (i.e. if the interest expense is 100 rubles, the Russian company will save on income tax 100 * 20% = 20 rubles, and the net expense will be 80 rubles).

However, not all so simple. The Tax Code of the Russian Federation provides special rules that do not allow companies to abuse this situation and completely remove interest on loans from foreign owners from Russian taxation. These are the rules of insufficient (or thin) capitalization (clauses 2-4 of Article 269 of the Tax Code of the Russian Federation) - conditions under which interest on a loan from a foreign owner is equal to dividends for tax purposes and, accordingly, is not deductible from a Russian company ( i.e. they do not reduce taxable profit) and are subject to withholding tax on dividends.

The first condition, the fulfillment of which threatens to turn interest on a loan into dividends for tax purposes, is the presence in the transaction of a foreign owner who directly or indirectly owns more than 25% (more than 20% according to the old rules) in the capital of the Russian company-borrower. In this case, the debt is considered “controlled”, i.e. simply suspicious (not to be confused with controlled transactions under transfer pricing rules - this is a completely different story). Let's consider the main situations when debt can be considered “controlled”:

1. If a loan was received by a Russian company from a foreign owner who directly or indirectly owns more than 25% (more than 20% according to the old rules) of the capital of this Russian company (see example in Figure 1):

2. If the loan was received by a Russian company from a company that is interdependent with a foreign owner who directly or indirectly owns more than 25% (more than 20% according to the old rules) of the capital of the borrowing company. (see example in Figure 2).

3. If the loan is guaranteed/secured by a foreign owner who owns more than 25% (more than 20% according to the old rules) of the capital of the borrowing company, or a company interdependent with the foreign owner (see example in Figure 3).

The second condition that must be met in order for interest on a loan to turn into dividends for tax purposes is a significant, more than 3 times (for banks and leasing companies - more than 12.5 times) excess of the loan amount (outstanding “controlled debt” ") above the company's net assets.

Thus, if both conditions are met at the reporting date (the debt is controllable and exceeds the company's net assets by more than 3 times), it is necessary to apply the thin capitalization rules, i.e. for tax purposes, part of the interest will turn into dividends; taxable profit cannot be reduced on this part and dividend tax will need to be withheld from it (if the loan was provided by a foreign owner - Fig. 1, or by a foreign company interdependent with the foreign owner - Fig. 2, if the loan was provided by a Russian interdependent company - Fig. 2, dividend tax is not withheld).

How to calculate the amount of interest that the Tax Code of the Russian Federation requires to be equal to dividends? For this purpose, a special coefficient is used - the capitalization coefficient. The actual interest on the loan must be divided by the capitalization ratio; the resulting amount is the “correct” interest by which the Russian borrowing company can reduce its taxable profit. The remaining amount is “wrong” interest, which turns into dividends, like a carriage into a pumpkin. If net assets are negative, the entire amount of interest on the loan is equal to dividends for tax purposes.

RusCo LLC is a Russian company, 40% of the authorized capital of which belongs to another Russian company, OJSC RusHolding, and 60% belongs to a foreign company Company Ltd. On May 31, 2016, RusCo LLC received a loan from Company Ltd in the amount of $300,000 at 10% per annum. Interest is paid monthly on the last day of the month. Payments of the principal amount of the debt will begin in 2017.

As of June 30, 2016, the assets of RusCo LLC were 15 million rubles, and the liabilities were 10 million rubles. (including tax liabilities of 500 thousand rubles). The US dollar exchange rate as of June 30, 2016 was 65 rubles. per US dollar.

Let's calculate the amount of interest that can be deducted and the interest that must be equated to dividends for income tax purposes.

Let's check the first condition: a loan from Company Ltd is a controlled debt, since it was received from a foreign owner who owns more than 25% (more than 20% according to the old rules) in the authorized capital of RusCo LLC.

We check the second condition: the amount of controlled debt as of June 30, 2016 = 300,000 * 65 = 19,500,000 rubles. Net assets = 15,000,000 – (10,000,000 – 500,000) = 5,500,000 rubles. Thus, the amount of controlled debt is more than 3 times the net assets at the reporting date (19,500,000/5,500,000 = 3.5).

Therefore, in this situation it is necessary to apply the rules of thin capitalization.

The total amount of interest accrued for the second quarter of 2016 = RUB 160,274.

Capitalization rate = 19,500,000/(3 x 5,500,000*60%) = 2

Consequently, out of the total amount of accrued interest, RUB 160,274. only 80,137 rub. (160,274/2) can be taken as a deduction (reduce the taxable profit of RusCo LLC), the remaining 80,137 rubles. from 160,274 rub. are treated as dividends for income tax purposes, i.e. Dividend taxes will need to be withheld from this amount.

Transfer pricing