Franchising: Accounting and tax accounting of operations under a commercial concession agreement

To the question “What is lump sum? You can answer literally in a nutshell - this is the cost of the franchise.

For some, this answer may be sufficient, but a more curious and inquisitive person who is also planning to buy a franchise will not be satisfied with this simple explanation.

So what is a lump sum? How and according to what parameters is it formed? Is there a difference between a lump sum and a royalty? And how do they differ from each other? Why is the lump-sum fee for some franchises over a million, while for others it is not at all?

Let's try to answer these questions.

The lump sum fee is...

The etymology of the phrase “lump sum” in Russian business vocabulary is quite interesting.

Despite the fact that franchising in its modern form took shape in the United States, in the Russian lexicon the term that refers to the cost of a franchise in America is franchisefee(translated from English - license fee) - did not take root. Instead we use the German term die Pauschale, which in turn comes from the cognate der Bausch in translation meaning "a thick piece of something".

Even stranger is the fact that the definition of a lump sum fee, as in principle, and franchising, as a type entrepreneurial activity In general, there is no such thing in Russian legislation. However, the absence of these concepts in the civil code does not mean that franchising does not exist in our country or is not legalized at all. Franchising works in Russia, but is still regulated by a commercial concession agreement (Articles 1027-1040 of the Civil Code of the Russian Federation). There, in Article 1030 of the Civil Code of the Russian Federation, it is mentioned that a commercial concession agreement may contain a clause on the remuneration that the user (read “franchisee”) pays to the copyright holder (read “franchisor”) in the form of a one-time and/or periodic fixed payments (read “lump sum” and “royalties”).

Thus, lump sum is a fixed amount that the franchisee pays to the franchisor under a commercial concession agreement. In practice, this means that an entrepreneur, buying a franchise and concluding an agreement with the franchisor company, acquires the right to conduct business under the franchisor’s trademark, using its name, technologies, standards and products.

Lump sum and royalties

As mentioned above, a commercial concession agreement provides for both one-time, one-time payments and periodic ones. A lump sum payment is a one-time payment. I paid and forgot. It is also called the entrance fee or initial payment, since it is paid immediately after the conclusion of the commercial concession agreement. Only after payment of the lump sum fee does active interaction between the franchisor and franchisee begin.

Remember, the lump sum fee is not the only investment in a franchise business. Investments in starting a franchise business are not limited to just a lump sum fee. No one has canceled the purchase of equipment, the purchase of goods, payment of staff, rent, etc... You can find out what the initial investment will be spent on by requesting this information from a franchise representative at BIBOSS.

Lump sum payment: accounting entries

Like any other items of expenses and income, the payment of a lump sum contribution is reflected in accounting and taxation for both the franchisor and the franchisee.

The rules for reflecting accounting transactions of parties to franchising activities are based on the provision “Accounting for intangible assets” PBU 14/2007.

Let's consider the system of accounting and taxation of a lump sum contribution using the example of a company that has been developing according to the franchising system since 2006 and has more than 1000 franchised enterprises. The economic model of this franchise provides exclusively for the payment of a lump sum payment in the amount of 370 thousand rubles.

By the way, it should be noted that the activity under the franchising agreement is the main one for the 33 Penguins company, therefore the receipt of remuneration under the agreement - a lump sum - is reflected in the income from sales. If franchising is not the company’s main activity, the entry fee is reflected in operating income.

When receiving a lump sum payment, use accounting entries 51/62, 76, and upon payment 60, 76/51.

Speaking of payment. The accounting of the 33 Penguins franchisee takes into account the lump-sum contribution in deferred expenses on account 97 “Deferred expenses.” Further, the lump-sum contribution is applied in equal shares to expenses for ordinary activities during the term of the contract. In the case of the “33 Penguins” franchise - for 5 years.

In the future, the accounting departments of the franchisor and franchisee interact with each other within the framework of the “Supplier-Buyer” model.

Speaking about the taxation of a lump sum contribution, you need to keep in mind that for VAT purposes the provision of exclusive rights for use under a franchising agreement (commercial concession) is considered as the provision of services.

If the agreement is concluded on the terms of subsequent payment, then VAT is accrued on the amount of the lump-sum payment on the date the agreement enters into force. If the commercial concession agreement provides for payments in advance: a one-time payment - before the transfer of the right to use a set of exclusive rights; periodic remuneration - before the beginning of the quarter for which it is paid.

In this case, the copyright holder is obliged to calculate VAT on the date of receipt of the advance payment based on its amount and the calculated rate. Next, within five calendar days, issue the user an invoice for the advance received. After transferring the right to use a set of rights (for a one-time payment) or the end of a quarter (for periodic payments), the copyright holder calculates VAT on the entire amount of remuneration due and issues an invoice to the user. The amount of tax paid on the advance is deductible.

Seven guises of lump sum

So, in order to open a franchise business, an entrepreneur needs to pay a lump sum fee. It would seem that everything is simple, but it was not so.

If you study the franchise offers on BIBOSS, you will notice that the size of the lump sum fee varies from franchise to franchise - from 15 thousand to 2.5 million rubles- and sometimes it is completely absent.

For example, no lump sum fee Most clothing stores operate under franchising, as well as those companies for which franchising is a way to increase the number of points of sale of their products. The more franchise enterprises and the more goods they sell, the greater the production volume will be, which means the profit will increase. That is why it works well without charging a lump sum fee from its partners.

But if you look at a franchise as a product or service, then the lump sum fee serves as a price and is formed according to a certain pricing system. From this point of view,

The franchise has its own cost and markup, from which the lump sum fee is made up.

But you should also not forget about the markup on the product - the franchise. Let us remember the most important rule of pricing - this is the provision of a product or service at the price that the buyer is willing to pay, and at the same time will suit the seller. The franchise is no exception. A lump sum fee is the amount that an entrepreneur is willing to pay to start his own business under a certain brand and with the help of a franchisor. The higher he values the acquired capabilities, the higher the lump sum becomes.

In any case, the size of the lump-sum fee is determined by the franchisor company, so we invite you to familiarize yourself with the principles of forming the lump-sum fee of several companies.

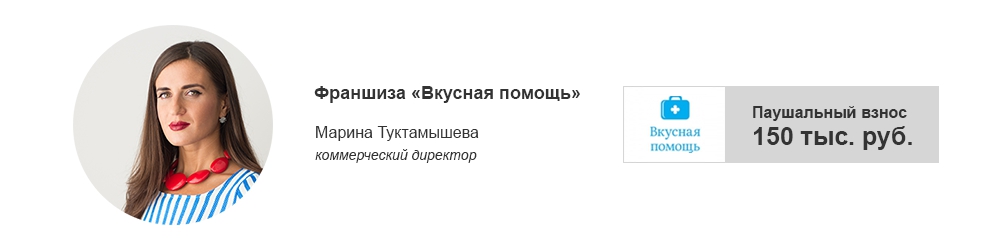

A lump sum contribution for our company is the amount that a partner pays for using the “Tasty Help” brand.

The lump sum contribution of our franchise can be called sufficient symbolic. This amount is specified in the commercial concession agreement, which is concluded for an indefinite period.

We created the franchise not for the sake of receiving a lump sum fee, but for the sake of popularizing our brand and increasing the points of sale of our products. This is why we do not increase the lump-sum fee, are loyal to our partners and are committed to long-term work.

We perceive the lump sum fee as a certain degree of seriousness on the part of the franchisee - his willingness to represent the brand and develop his business with us.

The absence of a lump sum fee is an additional advantage of the franchise offer. No lump-sum fee or royalty franchise over attractive and competitive in the franchising market.

Thus, the franchisee pays only for the volume of goods that is provided for by the supply agreement concluded together with the commercial concession agreement.

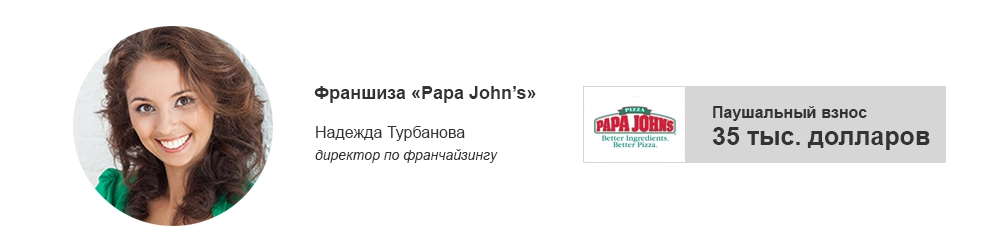

The down payment for purchasing a Papa John's franchise is 35 thousand dollars. First of all, the cost of the lump sum fee in dollars is due to the fact that PJWRI is developing the Papa John's master franchise, which means that PJWRI initially agrees on the amount of the lump sum fee, and also pays the copyright holder - the American company Papa John's - for opening each pizzeria opened by a sub-franchisee. And he pays in dollars.

It is logical that we also accept entry fees from our subfranchisees in this currency. This is what most international companies operating under franchising in Russia do in order to protect themselves from exchange rate fluctuations, which are so common in our country.

It is worth adding that the lump sum payment has a special economics of miscalculation. First of all, it is related to the expected profitability of the franchised establishment.

If we consider this issue in more detail, then, first of all, a lump sum fee is a payment for the right to work under a world-famous brand, for the technologies and recipes provided. But not only.

For example, the initial Papa John's payment, which subfranchisees pay, also covers the costs of PJWRI for conducting training for franchisees in Moscow, for the company's specialists to travel to the franchisee's city to open an establishment, for developing a restaurant layout and a marketing plan. In addition, after payment the sub-franchisee receives a ready-made lump-sum contribution, and most importantly, powerful sales tool- a website localized for each partner.

In order for a brand to become famous and generate considerable income, a lot of experience and financial investments into business. It takes quite a while for a brand to become famous. a large number of time.

Franchising is the next step in profitable investment. However, as with any type of business, there are certain risks that can affect the economic growth and development of a new enterprise. In this case, the amount of money received as a result of the sale of the franchise will partially compensate for the likely losses.

Types of franchise payment

Material compensation for the use of a trademark is stipulated in the contract and is made in different ways. Payment options depend on many factors.

The following franchise payment options are available:

- Lump sum payment.

- Monthly payments - royalties.

- Combined payments.

Legislative side of franchising

In most cases, when purchasing rights to use famous brands, you must pay an initial payment or lump sum. What is this? In simple words formulated as the basic price of the acquired business. The term comes from the German phrase der Bausch, although the origins of the franchise are American.

It should be noted that the legislation Russian Federation There are no terms of entrepreneurial activity under the franchising scheme. However, legal work is carried out legally regulated. According to one of the clauses of the document, the user can pay remuneration to the copyright holder in the form of regular or one-time payments.

Definition of down payment

Thus, what a lump sum fee is is defined as a certain amount that is paid to the owner of a brand according to a commercial concession agreement. In a practical sense, the franchisee, acquiring the right to business activity, uses not only the brand name, but also other marketing products developed by the company.

Quite a large number of entrepreneurs are now thinking about starting their own business, not under their own newly created brand, but under a fairly famous name.

However, there are a large number of pitfalls in the franchise that need to be sorted out before signing the appropriate agreement.

Lump sum payment

Businessmen who are thinking about opening their own franchise still cannot fully understand what the concept of a lump sum fee means.

In fact, this is not at all surprising, since this term came to the country from in English, which not everyone owns.

If we give the definition of such a contribution, it turns out that this is a real success of franchising.

Each franchise consists of a small number of parts, and one of them is just such a lump sum contribution.

A situation often occurs when fairly large enterprises turn to smaller ones for help to expand their own business. This type of cooperation is optimal for each party, as it brings mutual benefits.

The meaning of such a relationship is that a large businessman transfers his:

- Technology.

- Products.

- Services.

- Trademark.

At the same time, in mandatory it is required to draw up a mutual cooperation agreement, which provides for such a contribution.

The payment must be paid by the partner for the provision of services.

Lump sum payment

In fact, payment as a lump sum payment is used quite rarely.

Most often it is used only in certain cases, when the partner is not yet known on the market and therefore there are doubts that he:

- Will be able to implement correct implementation.

- Will be able to conduct a successful development release.

Quite often, the fee is used in a situation where it is not possible to control products released under a certain license.

Here the franchisor will not be able to obtain all the certain data necessary to make a correct calculation.

Most often, the payment accounts for twenty to twenty percent of the entire license price.

Lump sum tax

In addition to the lump sum payment, there is also another fixed payment, this is the so-called lump-sum tax.

Lump sum tax- This is a fixed payment, charged in certain amounts, which in no way depend on all kinds of economic variables.

Most often, the payment accounts for twenty to twenty percent of the entire license price.

In addition, it is also worth separately noting the fact that such a lump-sum tax can also be classified as a cost that does not in any way depend on the direct volume of total production.

Payment and postings

The wiring is varied:

- changes;

- entering size total installed capital.

These changes should be reflected directly in the process of directly providing all kinds of franchising services. Similar installed capital must be contributed by the junior partner.

By directly providing such services, franchising reflects all its movements with various entries, for example, contributions to capital.

All movements of such wiring must be supported by various documents.

In this case, the franchisor must take into account all capital movements, while providing all agreed services.

Lump sum and monthly royalties

Nowadays, building your business by purchasing a franchise is a popular way.

Along with the acquisition of such a franchise, the entrepreneur also receives a large number of various bonuses, to which include:

- Enough low price for goods, which will later be used to conduct business.

- All staff will be trained by experienced franchisees, and this will help the business develop, since only qualified people should work in trade and provision of services.

- Constant support from large company.

- A recognizable type of service provided or a well-known brand. Such an organization, due to its fame, will be provided with a constant flow of clients, which is a very important indicator for every businessman aimed at direct development and constantly growing income.

The optimal amount of contribution made, as well as royalties contribute competent and successful business development.

When purchasing a franchise, a partner must contribute a certain amount, and the lump sum contribution is a fairly large part of this payment.

The contribution is most often made only once. At the same time, it can be paid in installments, or it can be provided at once in a total amount. However, most often, large partners require payments to be made within a short time.

Here's the concept royalties can be classified as completely opposite types of payments. These payments must be made by the affiliate who purchased that particular franchise.

In this case, royalties can be of two completely different types:

- Fixed amount, which is stipulated in advance in the contract.

- A certain percentage, which is charged from the partner's profits.

To ensure the successful operation of their business, partners must choose the optimal royalty for them, the most beneficial for each party.

If the royalty is too high, then the certain profitability from this franchise will be quite underestimated. For this reason, the whole point of the business can quickly be lost.

To open your own business, when purchasing a franchise directly, it costs special attention pay attention to the contribution and the amount of the royalty in order to accurately determine for yourself how attractive and profitable this offer is.

Royalty rate

There is a huge difference between a contribution and a royalty, the first payment is determined directly by the big businessman himself, and the second represents a certain rate.

There is a huge difference between a contribution and a royalty, the first payment is determined directly by the big businessman himself, and the second represents a certain rate.

Royalty rate– this is a certain amount that is used as a reward to the owner for the use of his copyright.

This implies the fact that the partner under the received agreement is obliged to pay:

- Trademark.

- Brand.

It is worth noting that the established royalty price All sorts of extras are also included:

- Varied promotions.

- Price all marketing.

- Training costs personnel.

- Accommodation necessary information directly on the website of this brand.

Royalty calculations can be done in two different ways:

- A certain percentage of the stamp. This type is often used in situations where the store uses a variety of markups on a certain product.

- Fixed definite calculation. The payment is permanent and depends directly on the contract itself. The assigned amount largely depends on a large number of indicators, for example, on the area of the building used, the number of visiting and regular customers, and the cost of all franchising services. Most often, this type is used by companies for which it is quite difficult to calculate the entire amount of permanent income.

- A percentage calculated from the turnover of the entire enterprise. Now this type royalty is considered the most popular, since a certain percentage specified in the contract is calculated.

Royalty franchise

This concept means specific fee, carried out by a partner, for all kinds of real estate objects transferred to his direct ownership, as well as various technological devices.

Payment is made for obtaining the direct right to use a variety of positions that are protected by patents.

When purchasing a franchise, compensation must be charged for that the partner has full right to dispose of:

- Trademark.

- Logo.

- Slogan.

With this, you can attract clients, since you don’t need to spend a lot on developing or creating your brand.

Franchise without lump sum fee

Franchise means a certain set of rights of a specific enterprise to use the intellectual property of a completely different enterprise.

Such descriptions must be attached to the agreement concluded between two cooperating parties who are franchising among themselves.

Directly in the text of the agreement information must be provided about what concerns relationship between both parties.

If by agreement lump sum payment not specified, it means that a large company offers cooperation without a fee.

Thus, it attracts a large number of interested entrepreneurs who want to distribute goods.

In such a situation, so-called dealer relations, in which any one company will produce and wholesale various goods, and the other will distribute these products and sell them under the label of the manufacturing company.

Moreover, the full owner of such a product is always the franchisor himself, who can independently dictate all the rules for the procedure for selling products.

For the dealer himself, this agreement will also have a certain benefit, since he will not have any large expenses.

However, in such a situation it will be quite difficult for him to make a big profit, since most often the supplier of this product does not provide the opportunity to develop the business and increase profits.

* The calculations use average data for Russia

To date, Russian tax legislation does not contain any taxation features that are unique to franchising. This means that an individual entrepreneur who has entered into a commercial concession agreement, as in the case of opening own business from scratch, can choose between general and simplified taxation systems.

When choosing a regular (general) taxation system, an entrepreneur will pay the following taxes: income tax individuals(NDFL), value added tax (VAT), insurance premiums(former UST). Income received by a franchisee-individual entrepreneur is subject to personal income tax at a rate of 13% (Chapter 23 “Individual Income Tax” Tax Code RF). As in other cases of doing business, this type of tax is levied on all income received by the franchisee from conducting their business activities, reduced by the amount of actually incurred and documented expenses that are directly related to the receipt of these incomes (the so-called professional tax deductions). Costs include insurance premiums paid. The taxpayer himself determines which deductible expenses should be indicated in the declaration in the same manner as expenses are determined for tax purposes in accordance with the chapter “Organizational Income Tax.”

The main expenses that may arise for an individual entrepreneur in the process of executing a commercial concession agreement are the costs of state registration franchising agreement (including state duty), expenses for remuneration to the franchisor (royalties and lump-sum fees are included in the same way as expenses associated with production and/or sales), expenses for training of the franchisee (if training fees are allocated in the agreement separately from the lump-sum fee and is paid separately), expenses in the form of the purchase price of goods that are purchased by the franchisee directly from the franchisor or other suppliers (but only if the franchisee subsequently resells them as part of his business activity), expenses for advertising products that the user sells or produces, the services he provides or the work he performs. Advertising expenses are also often included in the royalty amount, which is understandable, since the franchisor has a direct interest in stimulating sales of products under its brand. However, if there are advertising campaigns initiated by the franchisor, the franchisee also has the right to advertise its activities in the region where it operates. In this case, his advertising expenses reduce the tax base.

In accordance with subparagraph 20 of paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation, a franchisee under the simplified taxation system may include as expenses the costs of advertising manufactured or acquired and/or sold goods, works or services, a trademark or service mark. The accounting procedure is given in Article 264 of the Tax Code of the Russian Federation. Advertising expenses that are not mentioned in the code are recognized in an amount of no more than 1% of sales revenue, determined in accordance with Article 249 of the Tax Code of the Russian Federation.

Let us repeat that it is possible to take such expenses into account only if the entrepreneur can confirm all his expenses on paper. If he doesn't have necessary documents, proving the amount of expenses, then the professional tax deduction will be 20% of the total amount of income received by the beneficiary in the course of his business activities.

The franchisor's remuneration also includes value added tax (VAT). To do this, the user must have an invoice indicating the total amount of remuneration and the corresponding amount of VAT that the copyright holder gives him. According to Article 164 of the Tax Code of the Russian Federation, the VAT rate on goods and services throughout the country is 18%. However there is certain exceptions: individual products for children, separate foodstuffs, periodicals and book products of an educational nature, as well as certain medical products of domestic and foreign production are taxed at a rate of 10%. The amount of VAT on payments to the franchisor is deducted in the usual manner, which is regulated by Articles 171 and 172 of the Tax Code of the Russian Federation. The right to deduct the amount of VAT arises only after payment of the lump sum contribution. In the case of royalties, VAT can be deducted after each payment of remuneration to the copyright holder. Accordingly, tax deductions from the cost of other work or services that are necessary for carrying out business activities under a commercial concession agreement are also made in accordance with the provisions of Chapter 21 of the Tax Code of the Russian Federation.

Ready ideas for your business

The beneficiary, an individual entrepreneur, also pays insurance premiums (previously called the unified social tax), amounting to 34% of wages. For some types of activities, a preferential rate of insurance premiums is available (for example, for organizations operating in the field of information technologies or providing engineering services, companies that employ disabled people, and a number of other enterprises).

If an entrepreneur prefers a simplified taxation system (STS), then in this case interest rate taxes will range from 6 to 15% depending on the type of simplification. An additional advantage is the absence of transfers to extra-budgetary funds if the individual entrepreneur does not have employees. The tax is levied on income received by an individual entrepreneur during the tax period in cash or in kind, minus expenses used to generate profit. Expenses accepted for such deduction are determined by the provisions of Chapter 25 of the Tax Code of the Russian Federation. Expenses of taxpayers who have chosen the simplified taxation system are recognized as expenses after their actual payment, in accordance with clause 2 of Art. 346.17 of the Tax Code of the Russian Federation. And in accordance with paragraph 1 of Art. 252 of the Tax Code of the Russian Federation, income received can be reduced by expenses if the latter are economically justified, supported by documents that meet the requirements of the law, and incurred to carry out business activities to generate income. If the expenses do not meet at least some of these requirements, then it will not be possible to reduce taxable income.

In case of individual entrepreneurs operating under a commercial concession agreement, such expenses included in the costs include the cost of paying a lump sum fee and royalties, expenses in the form of the purchase price of goods purchased from the franchisor or other suppliers, and the cost of training for running a franchising business.

Individual entrepreneurs who have chosen the simplified tax system pay taxes quarterly. Thus, they must make four payments per year: for the first, second, third and fourth quarters, respectively. Payment for the first three quarters for individual entrepreneurs under the simplified tax system must be received no later than the 25th day of the month that follows the reporting month (that is, no later than April 25, July 25 and October 25). And the tax according to the simplified tax system for the fourth quarter of the reporting year is paid no later than April 30 of the following year. An entrepreneur can pay taxes by receipt through Sberbank or by payment through the current account of an individual entrepreneur or with the help of a client bank. The tax amount can be reduced by the amount of fixed contributions, but not more than half. This means that an individual entrepreneur using a simplified tax system of 6% can reduce the tax rate to 3%.

Ready ideas for your business

Since 2013, an individual entrepreneur can choose the so-called patent system taxation (PSN), which is a replacement for such regimes as simplified tax (USN), imputed tax (UTII) and agricultural tax (Unified agricultural tax). You can switch to a patent tax system with a tax rate of 6% voluntarily. In addition, it can be applied simultaneously with other tax regimes. However, for its application it is necessary that the average number of employees of the enterprise does not exceed 15 people, and the total revenue from the sale of all services and goods does not exceed 60 million rubles per year.

8 people are studying this business today.

In 30 days, this business was viewed 2496 times.

Recognizable brand. More than 330 partners in the Russian Federation and the CIS. Own production

according to European standards.

Ivan tea of Russia. Healing fees. Health know-how. Elixir of life.

Doing business in today's environment involves many risks and investments. But there is a way to reduce risk, reduce investments and time for the so-called promotion of a company, if you use franchising. Let's talk about this technology and find out its advantages and disadvantages.

Franchising concept

So, franchising is the organization of a business on the basis of an agreement, under the terms of which the franchisor company (product owner) transfers to the entrepreneur or franchisee company the rights to sell the franchisor’s services and product. In other words, the franchisor - the owner of the brand - on a contractual basis transfers the right to use a trademark, technology or other product successfully operating on the market. A franchisee can be an individual or organization that purchases a product and the right to use a brand on the basis of a concession agreement.

Terms of agreement

The concluded agreement provides for the following provisions:

- The franchisee company undertakes to sell the product using the seller's name, trademark, marketing technologies, advertising and support mechanisms, following the business rules established by the franchisor.

- The franchisor supports the franchisee by providing all the resources necessary to get started - advertising, material, consulting, and provides maximum discounts on the purchase of goods and equipment. The financial costs of preparing and opening a retail outlet are borne entirely by the franchisee. Such an agreement is called a franchise and is defined as a ready-made business system that makes it possible for a company to start operating by making profits, bypassing the difficult initial starting stage.

Of course, all this does not happen for free. And here the obligations of the brand buyer, called lump sum and royalties, come to the fore. Now let’s figure out what the cost of a franchise agreement is made up of, what contributions and with what frequency will be required when concluding such an agreement.

Franchise: lump sum, royalties and investments

The use of franchising significantly reduces risks and guarantees a quick and successful entry into the market. The franchise has a certain cost, which includes:

- A lump sum payment, paid at a time and confirming the right to use the brand. Its size is established in the terms of the agreement depending on the degree of fame of the organization offering the franchise.

- A periodic payment called a royalty is paid to the owner of the trademark. This is a kind of analogue of rent, the amount and frequency of payment of which is also set by the seller.

A novice businessman should remember that, in addition to purchasing a franchise, he will have to make investments, including the acquisition of fixed assets (premises, equipment) and working capital. But often part of the lump sum fee covers the costs of supporting the opening of a business, staff training, advertising and legal support, as well as assistance in establishing accounting.

Lump sum payment

Let's define the essence of the lump sum contribution. This is the most significant payment as part of a franchise, giving and confirming the right to conduct trading activities under the franchisor’s brand, using its proven technologies and, of course, goods.

At its core, the lump sum fee represents the actual price of the purchased license. The main criterion for its size is the predicted economic effect calculated by the selling company. The lump sum payment is paid once in one amount. It is possible to use installment plans, but for a fairly short period of time.

Royalty payment: concept and meaning

In addition to the one-time fee, the franchisee, in accordance with the terms of the franchise, regularly pays the copyright holder monthly, quarterly or annual payments. This is a royalty. This payment is part of the income received by the brand buyer in the course of his own trading activities. Its amount can be stipulated under the terms of the contract in a fixed amount or as a percentage of gross income.

In order for the franchisee to operate effectively, the royalty payment should not be excessive, since in such cases the profitability of the enterprise decreases so much that there is no point in purchasing a franchise. The same criteria apply to the size of the lump sum contribution.

But an ill-considered small royalty amount will not allow the franchisor to effectively manage a network of companies, i.e., the key to franchising success is the optimal calculation of basic payments. Therefore, the question of what royalties and lump sum fees in franchising are can be answered this way: this is an indicator of the level of profitability from the franchise. Basically, it is the size of the royalty that determines the profitability of this acquisition.

Interaction of the parties

Ideally, each party in franchising pursues its own interests - making a profit, minimizing risks. The franchisee receives a profit in the process of activity based on the privileges acquired under the franchise, and the franchisor, who is interested in the high profitability of the company, receives a monthly remuneration in the form of a royalty payment.

Therefore, conscientious partners interested in each other do not inflate the amount of contributions, setting them on the basis of realistically predicted economic benefits, determined by calculation and based on the practice of sales already made. There are many examples of such cooperation in global business.

Therefore, conscientious partners interested in each other do not inflate the amount of contributions, setting them on the basis of realistically predicted economic benefits, determined by calculation and based on the practice of sales already made. There are many examples of such cooperation in global business.

So, we found out that royalties and lump-sum fees are remuneration from the copyright holder, paid by the buyer for the services of granting the right to use intellectual property.

In the accounting registers of both parties, the conclusion of a commercial concession agreement is reflected in balance sheet accounts 04 " Intangible assets" and 98 "Deferred income", for the amounts of periodic payments (royalties and lump-sum payments), accounting entries are made by debiting and crediting account 76 "Debtors and Creditors".